How does Genovo help you fulfil the FCA’s expectations when recommending replacement business – Part I

Simon Large

|

IMPORTANT – This user tip relates to an older version of Genovo. Although much of the content and many of the concepts still apply to the current version of Genovo, the screenshots and some instructions may no longer be accurate. |

Welcome to May’s User Tip blog. This month, following several requests, we kick-off the beginning of a three-part series where we take a deep dive into what replacement business is and how Genovo handles it.

Part One covers off what replacement business is, the regulatory expectations and how Genovo deals with client objectives.

Part Two is jam-packed with details covering how Genovo helps you highlight your analysis of the existing plan, any benefits and features that may be lost by replacing it, and any potential disadvantages resulting from the advice given.

Finally, Part Three delves into how Genovo handles comparison of charges, performance and, in the case of pension, any associated death benefits.

Susan Sample

To help explain, I’ve created a sample client to walk through the process, meet Susan Sample. Susan is 55 years old and is a finance manager at an architecture firm on £30,000 per annum. She is married to Simon Sample who is a 61-year-old ex-plumber who retired early due to back problems and purchased a lifetime annuity to provide a guaranteed income. They have one child who has just finished their degree and is living in rented accommodation with their friends whilst working in an entry-level position at a marketing company.

Susan has a pension with MacroPensions PLC that she has paid into for the last 30 years, resulting in a fund value of £400,000. The plan does not have any guaranteed benefits and does not allow for flexi-access drawdown.

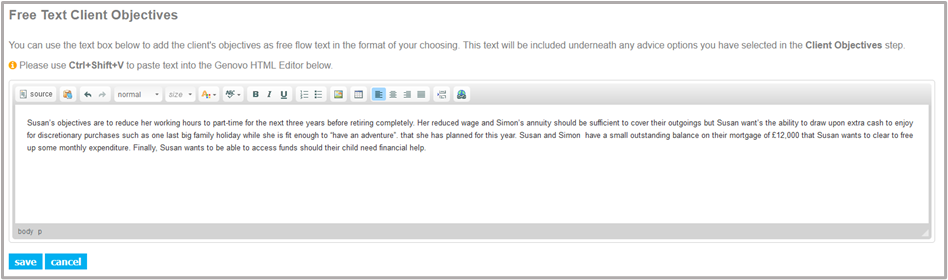

Susan’s objectives are to reduce her working hours to part-time for the next three years before retiring completely. Her reduced wage and Simon’s annuity should be sufficient to cover their outgoings but Susan wants the ability to draw upon extra cash to enjoy for discretionary purchases such as one last big family holiday while she is fit enough to “have an adventure” that she has planned for this year. Susan and Simon have a small outstanding balance on their mortgage of £12,000 that Susan wants to clear to free up some monthly expenditure. Finally, Susan wants to be able to access funds should their child need financial help.

We will advise that Susan switches into a modern personal pension plan with SuperPensions PLC which has the facility to allow Susan to flexibly access her retirement funds.

With Susan’s circumstances summarised, let’s begin looking at the theory and practice behind replacing her pension.

Part One – What, Why and How

What is replacement business?

In a nutshell replacement business refers to the process of recommending that an existing product or investment is switched, transferred or encashed and replaced with an alternative plan.

One notable point of contention is fund switches. There is some debate in the industry about whether fund switches are classed as replacement business, but at Genovo, in our humble opinion, funds switches do NOT qualify. Whilst there are still cost comparison disclosure requirements and you still need to ensure suitability for your client, we don’t feel you need to follow the full replacement business process when simply carrying out fund switches in isolation.

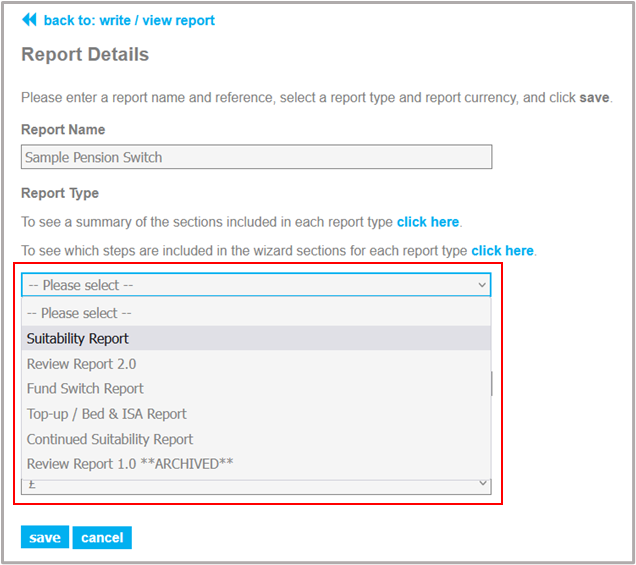

Genovo includes a variety of Report Types designed to cater for a slightly different advice scenario, but only the Suitability Report option can be used when recommending replacement business as this is the only Report Type that includes new product recommendation sections.

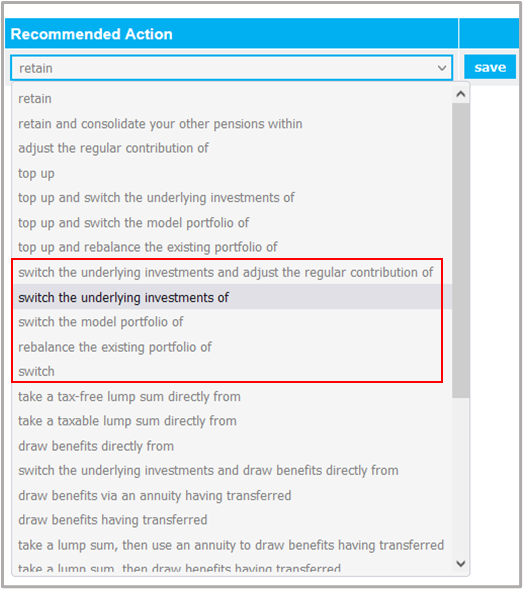

Whereas it is possible to recommend a fund switch in all Report Types, with the exception of the Continued Suitability Report, by simply selecting the appropriate Recommended Action in the relevant review section and including the revised investment strategy in the Recommended Investment Strategy section i.e. no new product recommendation is required.

The FCA requirements for replacement business

The FCA’s guidance regarding replacement business has changed little over the last decade with the key principles covered off in the FSA’s Finalised Guidance paper: ‘Replacement Business and Centralised Investment Propositions’.

Further guidance has been issued by the FCA during this time highlighting that when undertaking replacement business, you should ensure that you:

• Consider objectively your client’s needs and objectives.

• Collect necessary information on your client’s existing investments and the recommended new investments, such as the product features, tax status, costs and the performance of the underlying investments.

• Implement a robust risk-management system to mitigate the risk of unsuitable advice and poor client outcomes.

To sum up, you need to be able to demonstrate that the advice is suitable and, in the client’s, best interests. You need to be able to justify what you’re recommending and ensure that any potential disadvantages are clearly highlighted in the report – for example, any loss of benefits upon transfer or an increase in charges.

Client objectives

Given how essential client objectives are to a compliant suitability report, and the FCA have expressly stated in its list of good practice that:

“…including the client’s own words can be helpful as a guard against routine form-filling and making sure that the logic and direction of the recommendation is tailored to the client’s stated objectives.”

Let’s break down in detail how Genovo deals with them.

When creating a Suitability Report in Genovo you are always prompted, to confirm the client’s objectives in the Client Objectives step of the Introduction section. This step comes preloaded with several standard Advice Options designed to cover some of the more commonplace advice scenarios. However, given the FCA have, for some time now, highlighted the need to use client specific objectives and advised against relying on generic objective statements that frequently remain unchanged. How does Genovo handle this?

At this point, I would like to reintroduce Susan Sample and her goals and objectives that can be summarised as follows:

• Have the capability to withdraw a lump sum for a planned family holiday in the coming year.

• Clear the outstanding balance of £12,000 on her mortgage to free up monthly income as she reduces her working hours.

• Have access to additional flexible funds in case her child needs financial aid as they embark upon their new career.

• Retire completely in 3 years.

Genovo’s standard objectives are deliberately worded in such a way as to give them more of a client as opposed to a product focus.

Alongside this, Genovo provides three ways to input your clients’ objectives to demonstrate Know Your Client and what Rory Percival referred to as, the extra ‘colour and detail’:

1) Free text client objectives

Clients’ objectives can be added in the form of multiple paragraphs. Breaking down the client’s objectives into individual bullet points may not always be practical or the best way to present the information back to the client.

To assist with this, Genovo gives you the ability to add objectives in the form of free text, by clicking add objectives as freetext. Selecting this will direct you to a new page where you can input the client’s objectives as full text which is especially useful if the client’s objectives have already been provided to you in this format and you simply want to copy and paste them into the report.

2) Use Genovo’s standard Advice Options

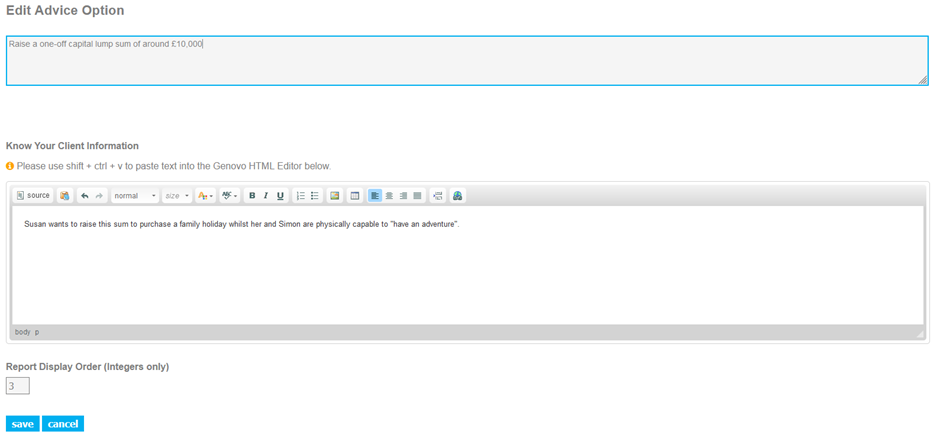

Secondly, as with any advice option or advice reason step in Genovo, the wording of the selected option is fully editable and can be further personalised to the client and their circumstances. This is achievable by selecting the add kyc info link in the furthest column next to a selected Advice Option.

You can utilise the freetext box beneath each Advice Option to add ‘colour and detail’ to the client’s objectives. You can also assign each of the objectives a Report Display Order so they appear in the report in the order of importance to the client. This is not only recognised as good practice by the FCA, but it also reaffirms to the client that you have listened, and you understand what is important to them.

3) Use custom Advice Options

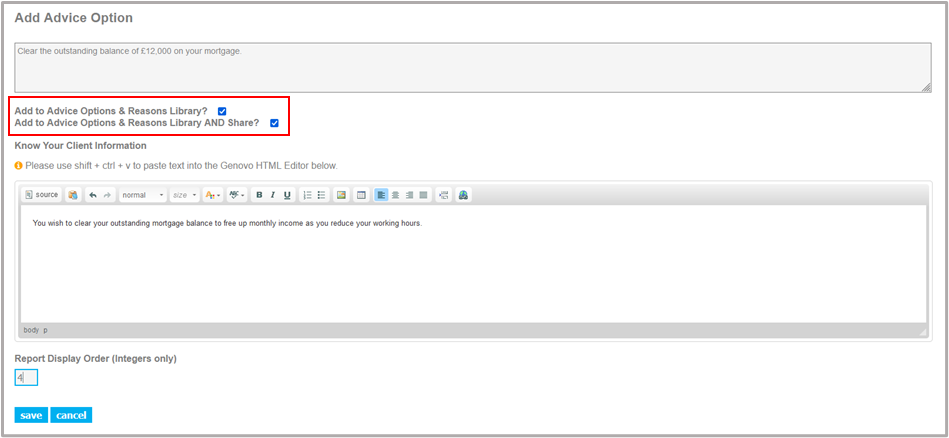

If none of the standard Advice Options are appropriate, or you simply wish to create your own, you can always add custom objectives by clicking add advice option. On this page, as with editing the Genovo standard Advice Options, you can also add some further information on the objective to ensure that it is client specific and add an order number to in-line with the client’s priorities.

Once you’ve added this information, you have the following options:

• Add the objective to this report and save it to your Advice Option and Reason library so you can select it in future reports.

• If you’re an Account Admin of a multi-user company plan, you can add the objective to this report, save it your library, and mark it up as shared by selecting Add to Advice Options & Reasons Library AND Share, so it’s then available for selection by you and all of your other account’s users or;

• Just add the objective to this report without selecting either option and then selecting save.

**As a side note – the adding of custom options is a feature you’ll see throughout Genovo and really allows you to go to town on personalising your reports.**

If you’re looking for further information about how to customise your Advice Options & Reasons, why not take a look at last month’s User Tip Blog where I go into more detail on how Genovo allows you to personalise your reports.

Spelling out the client’s objectives in one place will enable you to give them each due consideration to ensure the recommendations that follow are suitable. When adding the why’s, the what’s and the how’s to the rest of your report, make sure you relate them all back to the objectives recorded to show why your advice is suitable and to keep your compliance department happy.

That’s it for this month but please do keep a look out for next month’s user tip when I’ll be looking at how to add existing client plans into the Report Builder and how Genovo deals with inputting charges, plan features and benefits, and highlighting any potential disadvantages associated with switching the existing plan.

Further Reading

You’ll find loads more really useful information in:

• Genovo’s series of User Tip blogs;

• the extensive Genovo Knowledge Base;

• the collection of really useful Genovo matrices;

• the ever popular Genovo video tutorials; or

• by attending one or more of our regular monthly training webinars.

Of course, if you’re still stuck, or just need a helping hand, you can always submit a support ticket and we’ll get straight back to you.

Finally – make sure you don’t miss any of our hints & tips – subscribe and get email alerts when we update our blog.

Written by Simon Large

Simon is a technically minded individual with over 12 years experience working in the financial services with roles ranging from paraplanner, portfolio manager and adviser. He made the decision to change career paths into technology out of a genuine desire to help develop resources that result in better client outcomes. Outside of work, Simon volunteers his time mentoring future advisers & paraplanners with any time left over being reserved for studying and the occasional computer game binge.

Share this post

Free suitability report template

Learn how to make your reports more reader-friendly and engaging.

Suitability report best practice guide

Download the interactive guide and follow our 9 steps to better suitability reports.